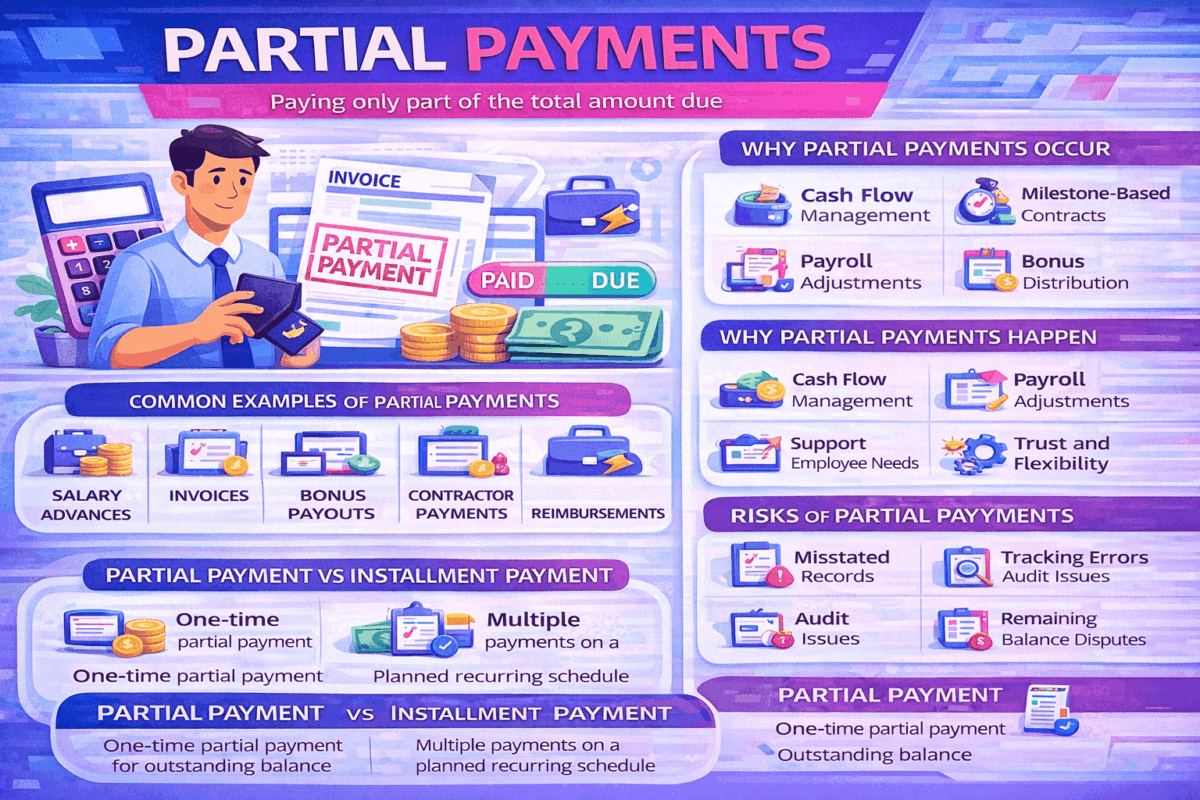

Partial payments happen when someone pays only a portion of the total amount owed, instead of settling the full balance at once. The remaining amount stays outstanding and is usually paid later based on agreed terms.

In HR, payroll, and accounting systems, partial payments are common. They show up in salary advances, contractor invoices, milestone-based vendor payments, bonus installments, and reimbursement processing. For organizations managing compensation, compliance, and financial reporting, partial payments are not exceptions. They are part of daily operations.

If the full amount is due but only part of it has been paid, that is a partial payment.

A partial payment occurs when a payer transfers less than the total amount required under a contract, invoice, salary agreement, or payment schedule.

For example:

In each case, the full obligation is not cleared with the first transaction. A remaining balance continues to exist until it is fully settled.

From a systems perspective, partial payments require accurate tracking of:

Without structured tracking, partial payments can create confusion in payroll reconciliation, tax reporting, and audit trails.

Partial payments are often intentional and operationally necessary. They usually occur for one of these reasons:

Organizations may stagger payments to manage liquidity, especially for large vendor contracts or seasonal revenue cycles.

In project-driven environments, vendors and contractors are paid based on deliverables. Payment aligns with completion stages.

Employee compensation can involve deductions, advances, retroactive corrections, or split payments across payroll cycles.

If part of an invoice is under review, the undisputed portion may be paid first.

Performance incentives are sometimes distributed over time to align with retention goals.

In modern HR and finance systems, partial payments are rarely accidental. They are built into compensation and vendor workflows.

In payroll environments, partial payments are more structured than in general invoicing. They typically involve:

Each of these scenarios affects compliance, taxation, and reporting. Payroll software must correctly calculate gross pay, deductions, statutory contributions, and net pay even when only part of the total compensation is disbursed.

For global organizations, partial payments also intersect with local labor laws. Some jurisdictions regulate how and when wages can be split or deducted. Accurate documentation becomes critical.

From an accounting standpoint, partial payments reduce the outstanding liability but do not close it.

If an invoice of $10,000 is partially paid by $6,000:

The same logic applies to payroll liabilities, contractor dues, and bonus accruals.

Modern finance platforms track partial payments using:

Clear records prevent revenue recognition errors and compliance risks during audits.

Partial payments can improve operational flexibility when managed properly.

They help organizations:

For employees and vendors, structured partial payments can reduce financial strain and improve trust.

When not tracked properly, partial payments can create serious issues.

Common risks include:

The problem is rarely the partial payment itself. The issue is the lack of visibility and documentation.

That is why most modern HR and finance platforms maintain automated ledgers, payment history logs, and real-time balance updates.

These terms are often used interchangeably, but they are not identical.

A partial payment is any payment that is less than the full amount due.

An installment plan is a structured agreement where the total amount is divided into predefined scheduled payments.

All installment payments are partial payments. Not all partial payments are part of an installment plan.

Understanding the difference helps in contract structuring and system configuration.

If your organization processes partial payments regularly, consider these guidelines:

Clear documentation protects both the organization and the payee.

Yes, in most commercial contexts. However, wage payment regulations vary by country and state. Employers must ensure compliance with local labor laws before splitting salary payments.

They can. Payroll taxes and statutory contributions are calculated based on gross earnings and payment timing. Systems must correctly allocate deductions across payment cycles.

No. The invoice remains open until the full balance is paid.

Yes. They are standard in payroll adjustments, bonus scheduling, reimbursements, and contractor compensation workflows.

Partial payments are a normal part of payroll and financial operations. They provide flexibility, support structured compensation models, and help manage cash flow. The key is not avoiding them. It is tracking them accurately.

When your HR and finance systems offer clear visibility into amounts paid, balances remaining, and compliance impacts, partial payments become manageable and predictable rather than risky.