House Rent Allowance, commonly known as HRA, is a salary component paid by employers to employees to help cover rental housing expenses. It forms part of the overall compensation structure and plays a significant role in payroll calculations and tax planning, especially in countries like India where HRA offers specific tax benefits under income tax laws.

HRA is not a reimbursement. It is a fixed allowance included in the salary package. However, a portion of it may be exempt from income tax if certain conditions are met.

For employees who live in rented accommodation, HRA can meaningfully reduce taxable income.

What Is House Rent Allowance?

House Rent Allowance is an employer provided allowance meant to offset the cost of rented housing. It is usually structured as a percentage of basic salary and is included in the Cost to Company package.

Employees who pay rent for residential accommodation can claim tax exemption on HRA, subject to rules defined under applicable income tax regulations.

If an employee does not live in rented accommodation, HRA is fully taxable.

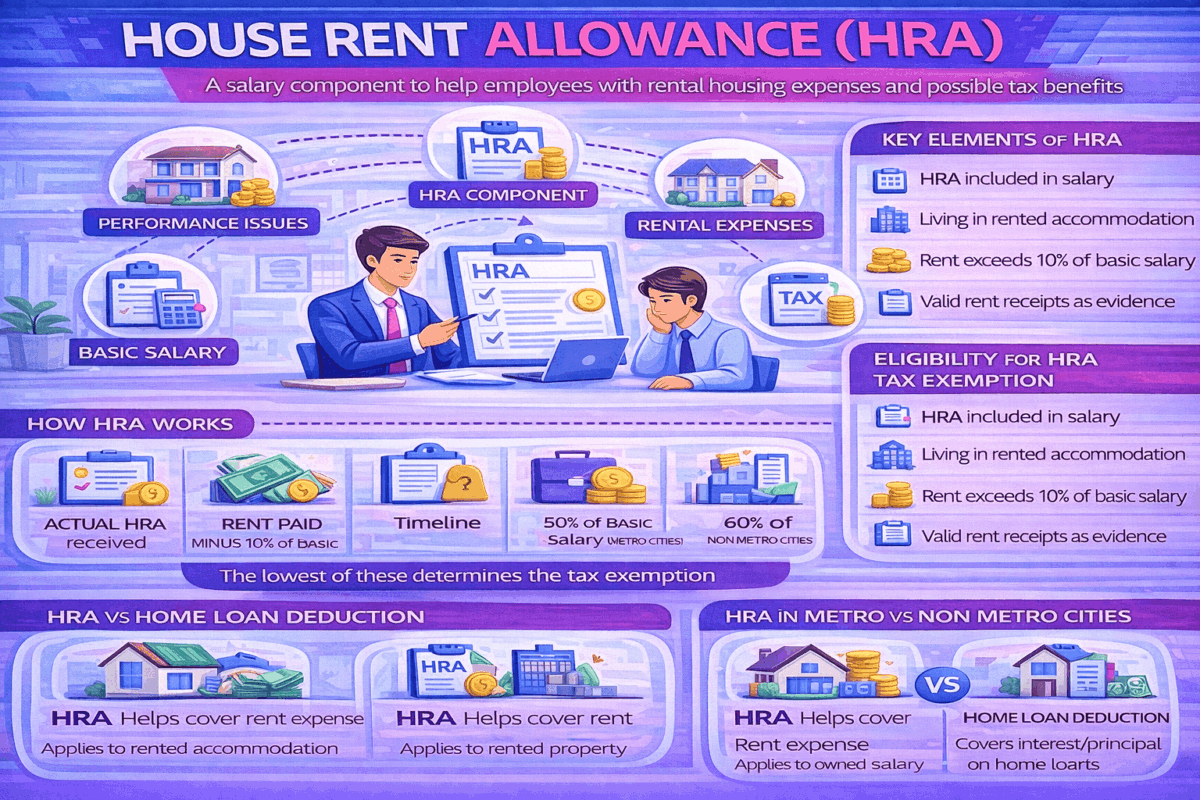

How HRA Is Calculated

In most payroll structures, HRA is calculated as a percentage of basic salary. Commonly, it ranges between 40 percent to 50 percent of basic pay depending on company policy and city of residence.

For tax exemption purposes in India, the exempt portion of HRA is calculated as the minimum of the following three amounts:

- Actual HRA received

- 50 percent of basic salary for metro cities or 40 percent for non metro cities

- Actual rent paid minus 10 percent of basic salary

The lowest of these three values becomes the exempt amount. The remaining HRA is taxable.

Because calculations involve multiple conditions, payroll systems must be configured accurately to avoid compliance errors.

Eligibility for HRA Exemption

To claim HRA tax exemption, employees must:

- Receive HRA as part of salary

- Live in rented accommodation

- Pay rent exceeding 10 percent of basic salary

- Maintain valid rent receipts or rental agreements

If annual rent exceeds certain thresholds, the landlord’s Permanent Account Number may also be required for tax documentation.

Employees living in their own house are not eligible for HRA exemption.

HRA in Metro vs Non Metro Cities

The tax exemption structure differs based on city classification.

Metro cities typically include major urban centers such as Mumbai, Delhi, Chennai, and Kolkata. Employees residing in these cities are eligible for exemption up to 50 percent of basic salary under the calculation formula.

In non metro cities, the applicable percentage is 40 percent.

This distinction recognizes higher rental costs in metropolitan regions.

HRA and the New Tax Regime

In India, employees now have the option to choose between the old and new tax regimes.

Under the old tax regime, HRA exemption can be claimed as per rules.

Under the new tax regime, most exemptions and deductions, including HRA, are not available.

Employees must evaluate which regime results in lower overall tax liability based on their salary structure and deductions.

Payroll teams should ensure employees are informed about these choices during tax declaration periods.

HRA vs Home Loan Deduction

HRA and home loan benefits are separate provisions.

An employee living in rented accommodation can claim HRA exemption.

If the employee owns a house and pays a home loan, they may claim deductions under home loan interest provisions instead of HRA exemption.

In certain cases, both benefits can be claimed if the owned property is in a different city and the employee rents accommodation at the place of employment.

Proper documentation is essential to avoid disputes during tax assessment.

How HRA Appears in Salary Structure

In a typical compensation structure, HRA appears as a distinct component alongside:

- Basic salary

- Special allowance

- Conveyance allowance

- Medical allowance

- Performance incentives

Because HRA affects taxable income, structuring salary with an appropriate HRA component can improve tax efficiency under the old tax regime.

HR and payroll systems must ensure accurate breakups to maintain compliance.

Common Mistakes in HRA Claims

Errors in HRA management often occur due to:

- Incorrect metro classification

- Missing rent receipts

- Claiming HRA while living in owned property

- Miscalculating 10 percent threshold

- Failing to collect landlord tax identification details when required

Automated payroll platforms reduce these risks by embedding tax logic directly into salary calculations.

Frequently Asked Questions

What is House Rent Allowance?

House Rent Allowance is a salary component paid by employers to help employees cover rental housing costs.

Is HRA fully taxable?

No. A portion of HRA may be exempt from tax if the employee meets eligibility criteria and follows prescribed calculation rules.

Can I claim HRA if I live with parents?

Yes, if you pay rent to your parents and maintain proper documentation such as rent receipts and bank transfer proof.

Is HRA available under the new tax regime?

No. Under the new tax regime in India, HRA exemption is not available.

What happens if I do not submit rent receipts?

Without valid documentation, HRA may become fully taxable.

Final Thoughts

House Rent Allowance is more than just a salary component. It is a structured financial benefit that affects both take home pay and tax liability.

For employees, understanding how HRA works helps in better tax planning.

For organizations, accurate HRA calculation ensures compliance and employee trust.

When payroll systems are configured correctly and employees submit proper documentation, HRA becomes a straightforward and beneficial component of compensation management.

Performance

Performance Learning

Learning Recognize &

Recognize & Engage &

Engage & Talent

Talent Innovative

Innovative Product

Product Learning

Learning Other

Other Featured

Featured